Guest written by Vincent Stevens, Senior Principle and Michelle Gwee, Senior Business Analyst at Delta Partners

Recognising the huge potential of OTT video in emerging markets, various players have made their forays in recent years – most notably with Netflix’s 2016 entry into markets such as India, Indonesia and Malaysia. While there are no clear signs of a winner yet, we have compiled the top four insights that traditional TV players, OTT players and telcos must bear in mind when catering to emerging markets.

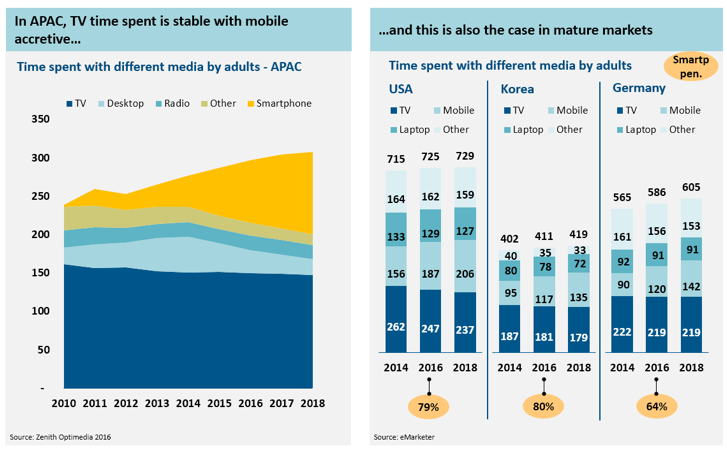

Insight 1: TV screen to remain dominant with mobile as a secondary screen

Although the prevalence of apps and smartphones has exploded in recent years, consumers are holding on to their time spent with a TV screen – even in developed markets (See Exhibit 1). Time spent on mobile devices is observed to be accretive and often a secondary screen while watching TV (sometimes passively).

Large screens like TV remain important for watching long-form video, while small screens (smartphones) are used to access short-form content. Unlike the rapid disruption of the internet on newspapers/print media, traditional TV appears more resilient to its OTT alternative. Main reasons are:

- Restrictive mobile data pricing for long-form streaming

- TV as a family entertainment medium in regions with large household sizes

- TV penetration exceeding smartphone penetration

As such, TV is expected to continue to command a dominant share in ad spend, as well as remain a key lever in telcos’ quad-play strategies for the next few years.

Insight 2: Local/regional content is king; Hollywood is queen

Despite the popularity of global hits such as House of Cards, audiences still demand localised content that they can relate to (or even understand – in the case of some emerging markets with low levels of English proficiency).

This is the case especially in emerging markets which tend to have strong local cultures and a strong local/regional celebrity following. For instance, ~80% of video preference is for Bollywood and regional content in India (See Exhibit 2).

Another example is Indonesia – which has a large Bahasa-speaking Muslim population (~90%) and regional celebrity K-pop and Thai celebrity craze in recent years. In its video app rankings, eight out of ten top apps are focused on such local and regional content. (See Exhibit 2).

Recognising the importance of local content, HOOQ provides quality local content on top of its international movies – via collaborating with leading production studios in Asia. Netflix has also been broadening its localised offering, for instance with Spanish-language “Ingobernable” and multi-national game show “Ultimate Beastmaster”.

Looking ahead, it will be interesting to see how OTT players balance the mix between a globalised and localised offering. The more localised/ authentic the content is, the narrower its potential audience base will likely be – hence compromising the business case for such productions or rights purchases. OTT players must carefully model out different scenarios and place selective bets.

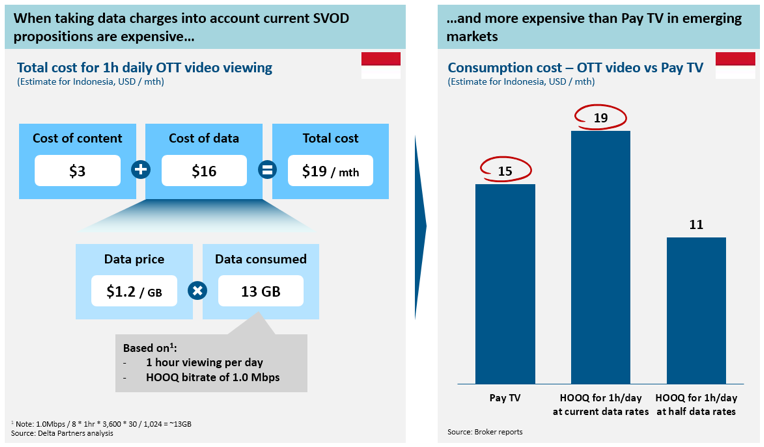

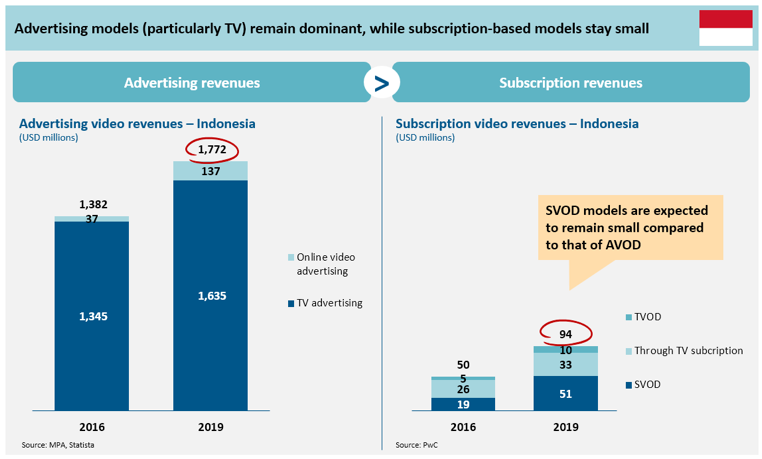

Insight 3: Advertising models rank ahead of subscription models

In emerging markets, SVOD models have yet to demonstrate long term financial sustainability:

- Poor affordability, after factoring in data cost. On top of monthly content fees, consumers must also pay for hefty mobile data charges – given that most do not have fixed broadband at home. This often results in the total cost of consumption for OTT video being even higher than Pay TV (Exhibit 3A).

- High piracy rates. Due to insufficient copyright law enforcement as well as inadequate IP rights education, piracy is especially widespread in emerging markets. With consumers used to getting content for free, there is a long way to go before convincing consumers to pay for SVOD price plans.

- Predominant focus on international content (See Insight 2).

TV advertising is still the predominant revenue engine for media companies today and the immediate future. For instance, the net TV ad market in Indonesia is at >USD 1,300 bn (2016) – versus ~USD 50 mn across subscription-based models. Feedback from advertisers is that TV advertising is to stay since it is the only truly mass market medium with “proven” performance ratings.

Additionally, free / ad-supported (AVOD) models such as YouTube have also thrived. It is projected that among AVOD, SVOD and TVOD models in emerging markets, AVOD will be where the bulk of the money lies (Exhibit 3B).

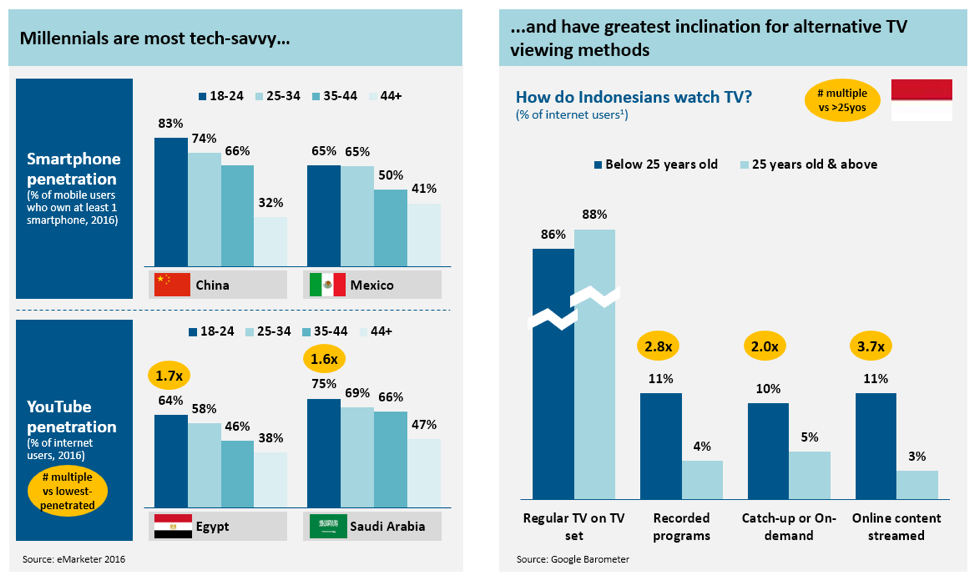

Insight 4: Millennials are different from Gen X

Generational differences between millennials and the older generation are crucial to understand – especially in emerging markets, which often have youth-centric populations. Millennials are undoubtedly the most tech-savvy group, with the highest smartphone and YouTube penetration rates (Exhibit 4).

In terms of TV behaviour, they are the quickest to catch on alternative forms of TV consumption (recorded, catch-up / on-demand, and online-streamed TV). As such, millennials are often naturally the first adopters of any OTT video proposition launched, making them a crucial segment to get right.

In terms of content preferences, user-generated videos are particularly popular among millennials. Today, there are almost one billion Pro-AM and Amateur content creators – including big YouTube stars like PewDiePie (who has more than 55 million followers), Raditya Dika and Kanan Gill – as well as a long-tail of amateur content producers. OTT players can hence consider strengthening up their content propositions with user-generated content – which could potentially attract youths more effectively (and more affordably) than expensive professionally-produced content.

In conclusion, OTT video in emerging markets requires a deep understanding of such ‘rules of the game’ and consumer preferences – as the first step towards capturing this dynamic and promising opportunity.